Asia-Europe air cargo market still in recovery

06 / 03 / 2023

Source: Cathay Pacific

The Asia-Europe trade lane has been buffeted by weakening demand and the outbreak of war in Ukraine over the last 12 months but there are some opportunities to be found.

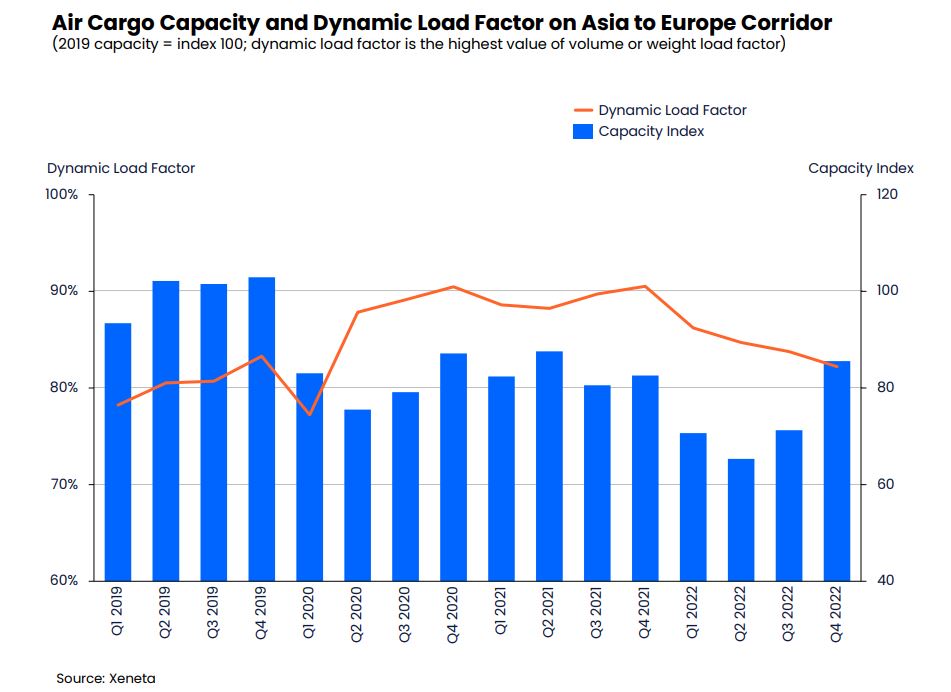

Air cargo capacity on the Asia-Europe route increased marginally (+3%) from the fourth quarter of 2021 to fourth quarter of 2022, but still remains about 18% below pre-pandemic levels, according to the ocean and airfreight rate benchmarking platform Xeneta.

This drop is also reflected in the balance with freighter cargo, with bellyhold freight making up just 32% of market share, compared to 55% before the pandemic, says Niall van de Wouw, chief airfreight officer, Xeneta.

The stricter Covid rules and lockdowns in China have slowed the return of passenger flights between Europe and Asia “so we don’t see the same level of recovery as we do on the transatlantic for instance”.

Russia’s invasion of Ukraine has also affected the route, especially into north east (NE) Asia where flights have traditionally flown over Russia.

“We saw prices on Europe – NE Asia route go up very quickly. There was an immediate boost in airfreight rates within a matter of weeks of the war starting,” says van de Wouw. “No doubt higher fuel prices were also a factor, but it is difficult to single out the cost of fuel on its own. And we also saw airline casualties, for instance”

He says that rates are now declining but that Asia-Europe rates are declining more slowly than on the Asia-US route.

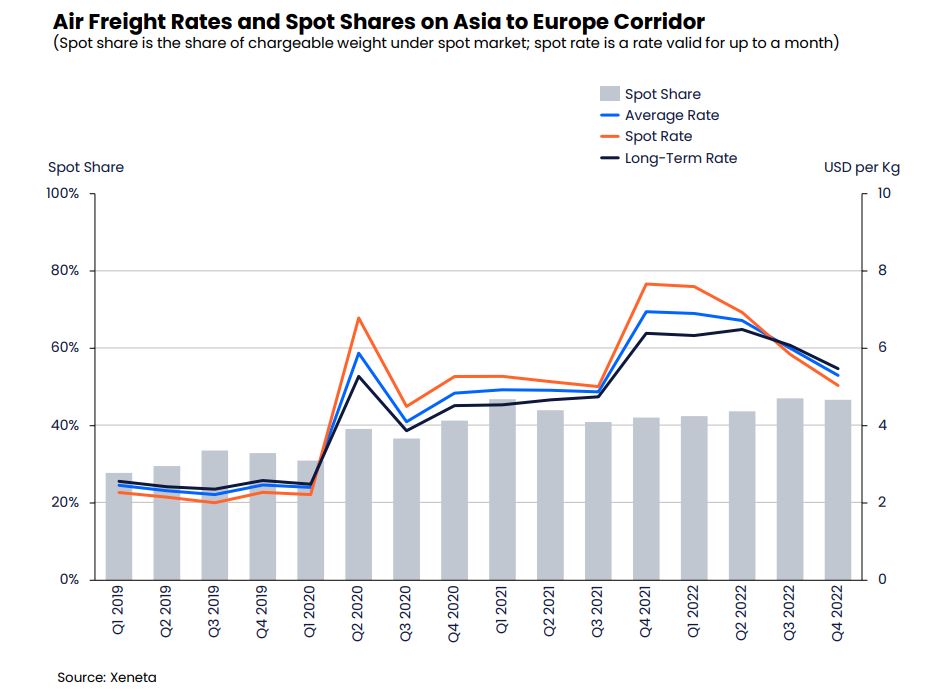

It is notable that in fourth quarter 2022, the spot market accounted for 47% of Asia–Europe volumes. It was 42% in quarter four 2021 and about 33% pre-pandemic.

“The market has been more short-term driven from a price point of view. Our best guess is that there has been so much uncertainty in the market that people are not willing to commit for longer periods of time,” explains van de Wouw.

The spot market is defined as rates valid for less than a month. Other cargo is carried under Block Space Agreements (BSA) and there are longer term rates that could be negotiated against capacity agreements or not.

It is evident that there is softening in the market, as spot rates fell below seasonal rates at the end of last year. “This is unusual – you only see that in a market downturn. Seasonal rates will then follow the downward trend.”

But this is not unexpected as more capacity means a decline in load factors, and so rates falling. Van de Wouw said there were three phases in 2022:

– Quarter one was very busy, with high load factors and strong negotiating positions for airlines.

– Quarter two and three saw a gradual decline in demand and lower load factors, which helps forwarders.

– And quarter four saw rate declines speed up.

Kelvin Leung, chief executive, DHL Global Forwarding Asia Pacific, says that over the last year, softening cargo volumes and gradually improving capacity led to reduced cargo load factors which indicated a demand-supply balance on European Union-Asia Pacific trade lanes.

“Capacity for December 2022 reached the highest level throughout the year, around 20% higher than the first half of 2022.

“Since the Lunar New Year holidays at the end of January 2023, we have seen some aggressive spot market rates across the trade lanes to Asia Pacific. We expect to recover in the long term towards the second half of 2023.”

Modal shift

Demand for airfreight capacity has also been affected over the last twelve months by the gradual improvement in ocean freight reliability and a subsequent fall in rates.

Tom Owen, cargo director, Cathay Pacific, agrees: “Seafreight rates have fallen very significantly and reliability has increased, so air is not as attractive as it once was. He adds that seafreight rates were probably artificially low before Covid and then artificially high during pandemic.”

He believes that the drive from sea to air has largely passed as capacity returns and congestion lessens on ocean services, “though some electronics, garments, vaccine and other related bio-products may continue to use airfreight as they have seen the advantages it brings”.

Twelve months ago, Cathay Cargo was not flying into Europe at all, so a lot has changed for the Hong Kong-based airline in the last year.

“We couldn’t operate to Europe for three or four months at the beginning of 2022 because of the Hong Kong SAR government’s Covid-19 restrictions on airline crew,” explains Owen.

In fact, flights were severely restricted throughout the pandemic, with just a skeleton schedule to European airports.

“Basically, we missed a lot of the issues around the restart of supply chains in Europe as we could not fly there,” he says.

Capacity has slowly grown since the middle of last year and all restrictions on pilots were finally lifted at the end of 2022.

Cathay Cargo is now operating widebody services to Frankfurt, Amsterdam, London, Paris and Manchester so the opportunity to lift more cargo continues to grow.

“We are targeting London in particular and hope to have four or five flights a day there by middle of the year,” he says. “It was one a day in quarter four last year and earlier it had been just one or two a week.”

China’s reopening

Owen says that China is reopening to the world but there are still significant challenges in the supply chain in the short term, with Covid rates initially increasing in China as it lifts restrictions.

The airline more than doubled its passenger flights into the Chinese mainland from mid-January, operating 61 return flights per week between Hong Kong and 13 mainland cities. It will reach more than 100 return flights a week to 14 locations by February.

“Our focus is the Chinese mainland. It has basically been closed for passenger aircraft from Hong Kong for the last two years,” he says. “The opening up will allow Hong Kong to function as it should for getting Chinese goods to the rest of the world.”

Tom Owen, Cathay Pacific Cargo

Cathay Cargo recognises that the market is weaker than it was – “the yields are softening for sure” – but sees opportunities to grow volumes, particularly in the areas of pharmaceuticals and temperature-controlled cargo as well as general cargo.

“We have opened a very significant cold chain facility in the Cathay Pacific Cargo Terminal – which doubles pharmaceutical-handling capacity. We are building on the back of our success moving vaccines during Covid,” he explains.

Owen says the airline is a classic combination carrier, and is seeing a continued lift in both freighter and widebody capacity.

“The frequency of the wide body scheduled services is very attractive to our ecommerce, post and mail customers, while the freighters can offer a more specialist service,” says Owen.

He explains that now that pilot restrictions have been lifted, the airline will have more flexibility and, for instance, will be able to quickly redeploy freighters.

“We can be more agile which is terribly important in this market. We can promise a route and deliver that route,” he says.

Finding opportunities

For Kuehne+Nagel Air Logistics, there are always growth opportunities in changing environments, according to Kenzo Yamada, vice president, air logistics development, Kuehne+Nagel Asia Pacific

“The reopening of China, the flourishing of new manufacturers in Southeast Asia and India, and the increasing demand of the Asian consumers are only some of the opportunity areas we are looking at,” says Yamada.

He admits that there have been challenging times. “We have lived under constant and rapid change in 2022 … with rates reacting to constant disruptions such as port congestion and Covid-19 pandemic consequences.

“The geopolitical tensions, and very specifically the tightening of global financial conditions that they brought, provoked a decline in air cargo demand during most of the second half of the year and that alone is a big change after several years of steady air market demand growth.”

He adds: “The largest impact on the rate development, we observed, was related to the fuel crisis driven by the war in Ukraine as the airfreight rates peaked. Additionally, extended flying time due to the war situation drives less payload, higher fuel costs and slower turnaround of the aircraft.”

Looking ahead, DHL’s Leung says that rates are coming down and that there are opportunities ahead.

“Rates will likely move towards pre-Covid levels however costs for air cargo carriers have been significantly impacted by inflation, fuel, ground and general operating cost,” he says.

“The situation, however, is fluid in terms of capacity and demand. There is also the unknown factor of how trade lane congestions will play out with further pandemic-related disruptions.

“On a positive note, China is opening up and we expect domestic economic activities to boost further in the coming weeks and months.

“Therefore, we expect imports into China to grow, especially with consumer products such as branded commodities.”

He adds: “We also see a higher demand for environmentally greener routes, such as multimodal transportation air-sea from European Union to Oceania destinations, and vice versa from Asia Pacific to the European Union as a sea-air product.”

Wenwen Zhang, airfreight analyst at Xeneta, said that despite the opening up of China at the end of 2022, with the removal of most Covid restrictions, Xeneta does not expect a recovery in the first quarter of this year.

“The outbreak of Covid (though it looks like it is passing its peak) and Chinese New Year means things will not change too quickly. International passenger numbers into China last year were down 98%, so will take some time to recover, but does mean every quarter we will get more and more bellyhold capacity.”

Wenwen Zhang, Xeneta. Photo copyright: Charlotte Wiig

Cathay’s Owen says: “We hope to be back to 80% of pre-Covid cargo capacity on Asia-Europe by the end of the year. We will grow in Europe with our partners Lufthansa and Swiss, where we have a big opportunity to co-ordinate schedules and sales activities.”

He is confident that China will remain a vital source in the supply chain despite the calls for more near-sourcing after the pandemic highlighted the challenges of relying on complicated and lengthy international logistics services.

“China is so integrated into supply chains that it would be pretty difficult for companies to extract themselves. It is a tried and tested system. It would take significant political willpower to change that.”

And he points to developments that are an example of the confidence that there is in Hong Kong as the gateway to the world – a third runway opening in 2025 which will help build more freight connections to the rest of the world.

And the establishment of the Hong Kong International Airport Logistics Park at Dongguan to the north of Shenzhen, which will offer an upstream but airside intermodal cargo-handling facility. Cargo will be taken by boat to a dedicated pier at the airport and loaded directly onto planes.