Unexpected airfreight rate stagnation down to fuel prices and a slowing market

07 / 07 / 2022

Image: Shutterstock

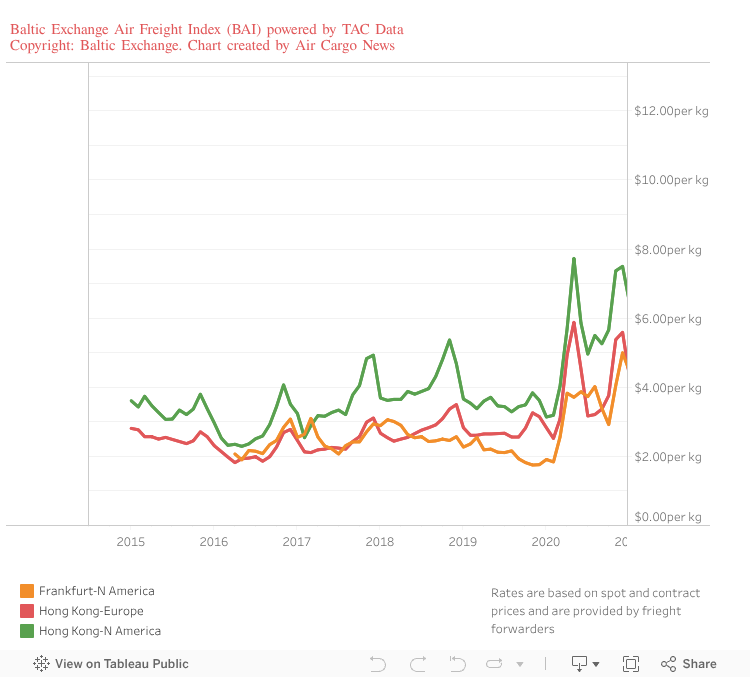

Many had expected the opening up of Shanghai and Hong Kong following strict Covid lockdowns to result in a surge in rates from Asia as factories played catch up following months of closure.

However, TAC Index figures show that rates actually declined marginally in June compared with May from Hong Kong to Europe and North America and from Shanghai to North America, while there was only a slight increase from Shanghai to Europe.

Writing in his monthly column in the Baltic Exchange newsletter, senior analyst at investment bank Stifel Bruce Chan – who had previously predicted rate increases following the lifting of Covid restrictions – said there were four possible reasons for the rate stagnation.

He said that a seasonal summer slowdown in demand could have kept pricing stable while a recent decrease in the cost of jet fuel could have helped mask any increase in the base rate.

Meanwhile, the rising cost of living and a slower than expected recovery in manufacturing capacity following the lifting of restrictions may also have had an impact.

“There’s the possibility that demand is starting to moderate on a longer term basis,” he wrote. “Are we seeing signs that the recessionary boogeyman has arrived? Airfreight volumes and airfreight rates are likely leading indicators, in our view, but we don’t have clear evidence to support that thesis.

“Annualised US GDP contracted 1.6% in 1Q22, for example, but unemployment and absolute consumer spending figures have been more resilient, and US inventory to sales ratios remain near all-time lows.”

He added: “While we do expect a broader slowdown at some point in 2023, we believe that what is currently impacting rates is shorter term in nature.”

Peter Stallion, head of air and containers, at derivatives broker Freight Investor Services pointed out that rates for the year so far had not eased off as much as many were expecting following last year’s highs.

He said: “2022 is on course for airfreight’s second-best year despite the softening of the market since the Covid policies have largely been repealed.”

He added: “Prices have certainly been tapering off – not boding well for the freighter market even with the destruction of available capacity [due to the sanctions-related grounding of AirBridgeCargo, CargoLogicAir and CargoLogic Germany].

“Moving forward, passenger freighters have seen far less prevalence (Etihad the latest airline to end mini-freighter operations to China), whilst the cyclical nature of air cargo had not really been a factor whilst the sector steamed through the 2020-2021 markets driven by COVID related demand and disruption.

“With this in mind, there may be more than a few businesses loaded with risk should the airfreight bubble burst.”

Etihad Cargo to end mini-freighters to China as flights ramp up