Airfreight rates expected to remain elevated in 2021

08 / 01 / 2021

Airfreight rates are expected to remain elevated in 2021 as the demand outlook remains uncertain and belly capacity is slowly re-introduced into the market.

Writing in a Baltic Exchange market update, Bruce Chan, vice president – global logistics at investment bank Stifel, said that airfreight rates are likely to remain elevated and volatile for some time, and those looking for reprieve in 2021 may have to be patient.

Chan said that a lack of bellyhold capacity would drive the high rates as passenger airlines will only slowly re-introduce international widebody services.

“By the second half of 2021, we do anticipate passenger flights to resume, especially as vaccinations pick up,” he said. “But we caution against over-exuberance, as the first flights to come back are likely to be short-haul, domestic, and leisure, which align less favorably with cargo.

“Core long-haul international travel and the belly capacity that comes along with it will be slower to return, in our view, so capacity relief for cargo should lag the recovery in airline passenger activity.”

Chan said that extra freighter and PAX-freighter flights would help alleviate some of the capacity pressure, but there were limits.

He explained that in the short term rates may not always be high enough to justify PAX-freighter flights, while in the long term companies may be cautious about investing in freighter conversions because of concerns about what will happen when belly capacity is eventually ramped up.

On the demand front, Chan said that a faster than expected rise in e-commerce demand, Covid-19 vaccine supply chains and PPE demand would all drive the airfreight market over the coming year.

However, he added: “The full impact of vaccine distribution on air freight capacity may not be as severe as some anticipate, due to the disbursed nature of production and, quite simply, the form factor of the doses—we believe the bottlenecks are more likely to come from container availability, storage, handling, and road distribution.”

With an uncertain rate outlook, shippers are looking to index-linked contracts and ad hoc agreements, according to Peter Stallion of air cargo derivatives broker Freight Investor Services.

“Much of the calendar 2021 pricing (full calendar year contracts) has reverted to a toss-up between the old normal for annual pricing and block-space agreements, to the new normal of high market-based price heavily focused on ad-hoc agreements.

“Unsurprisingly, a renewed focus has been placed on both index-linking of contracts in 2021, and dynamic pricing fed through and driven by airlines and forwarders to try to operate more efficiently to the elapsing market. Both of these factors have been driving [derivatives] interest.”

Summing up the air cargo market in the year ahead, Stallion said that on top of the challenges of low passenger volumes and lockdowns, rates now contend with an influx of Asia outbound vaccine cargo, the ups-and-downs of the Brexit agreement and a new strain of Covid “throttling cross-border commerce”.

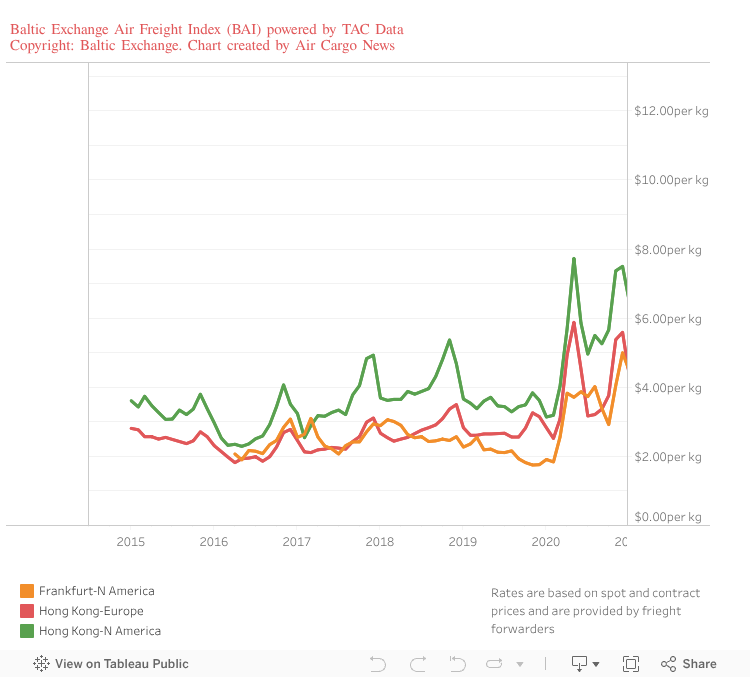

Last year, airfreight rates on major east-west trade lanes ended on a high. Data from the Baltic Exchange Airfreight Index (BAI) — powered by Tac Index — show that in December average prices from Hong Kong to North America were up 107.2% year on year at $7.50 per kg.

From Hong Kong to Europe average rates increased 77.5% compared with a year earlier to $5.59 per kg. And from Frankfurt to North America there was a 184.1% increase to $5.00 per kg.

Tac Index business development director Robert Frei said the price increases came on the back of an extended peak season with volumes in December up by 10% compared with a year earlier.

This resulted in aircraft utilisation levels reaching a record high in the middle of the month.

“The volume we saw is due to stock replenishment and we assume also in anticipation of further Covid-related lockdowns but it came alongside reduced supply in December,” he said.

“The annual Christmas vacations did not occur in the usual numbers meaning that the additional belly capacity was not seen this year.

“December numbers are therefore a result of fairly strong demand in relation to reduced available capacity.”

“Overall December pricing held up or even increased compared with November pricing. So the expected drop after the ‘peak season’ did not materialise in 2020.

“In December, no major impact from the ‘vaccine’ shipments was obvious. It remains to be seen whether this shall have a significant impact in January.”

Overall, BAI data shows that rates from Hong Kong to North America increased by 55.1% year on year to $5.49 per kg last year, while prices from Hong Kong to Europe were up by 46.2% to $4.02 per kg.