Airfreight rates slide in April

05 / 05 / 2023

Image: Shutterstock

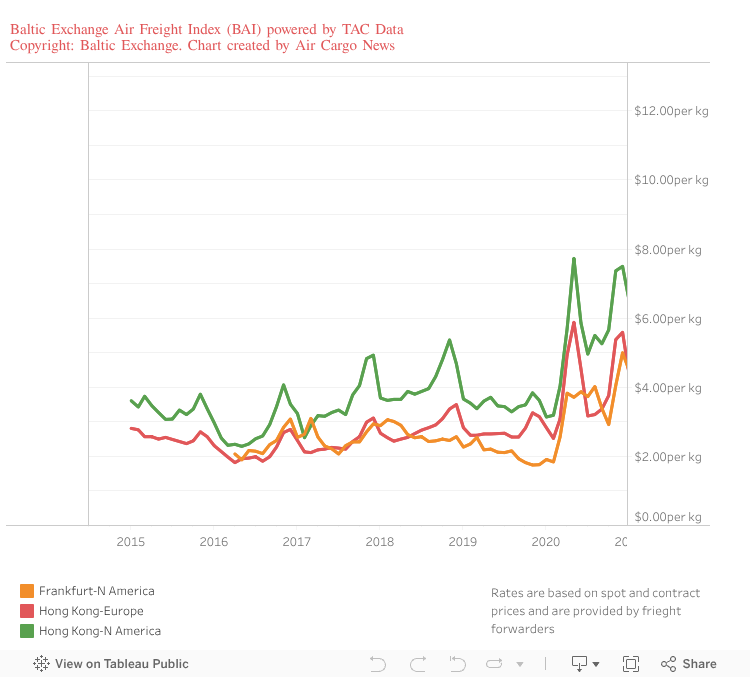

Airfreight rates on major east-west trade lanes declined in April as indicators of a recovery in March showed signs of fading (see chart below).

The latest statistics from Baltic Exchange Airfreight Index (BAI) show declines in prices between Asia and Europe, Asia and North America and across the Atlantic.

The falls are unusual as rates tend to rise slightly – or at least stay flat – in April compared with March.

The average price paid by forwarders – across contract and spot rates – on services from Hong Kong to North America declined to $5.20 per kg in April compared to $5.38 per kg a month earlier.

Against last year, rates on the trade are down 45.7% but they remain above the $3.60 per kg registered for the month in pre-Covid 2019.

It was a similar trend on services from Hong Kong to Europe where rates declined to $3.99 per kg in April compared with $4.15 per kg in March.

April’s rates on the trade are down 33.6% compared with last year, but are above the $2.65 per kg registered for the month in 2019.

Frankfurt to North America saw average prices in April fall to $3.08 per kg from $3.37 per in March. April’s rates are 43% down on a year ago, but are ahead of 2019’s $2.19 per kg.

Market indicators had suggested that the market may have been seeing a slight improvement in the early part of the year, but the drop in rates suggests this development eased in April – at least temporarily.

Bruce Chan, director and senior research analyst covering global logistics and future mobility at investment bank Stifel, recently highlighted the cloudy outlook.

“As we look out over the next year, there are several countervailing factors to consider, in terms of likely magnitude and even timing,” said Chan.

“On the demand side, supply chain congestion has abated, which means less need for expedited freight. But consensus continues to build around the likelihood of a 2023 inventory restocking, which, even if mild, may see the re-emergence of a peak season.

“All the while, logistics networks are realigning as shippers seek to diversify production sources across suppliers and geographies after three years of hard-learned lessons on supply chain resiliency.

“And finally, looming in the background of all of these demand discussions is what we see as significant, residual tail risk—factors that may not be extremely likely, especially (hopefully) from a geopolitical, multi-national conflict, or global financial institutional stability angle, but could produce significant disruption to the macro picture.”

IATA was similarly downbeat for the short term in its recent market assessment, although more positive for the latter part of the year.

IATA director general Willie Walsh said: “Air cargo had a volatile first quarter. In March, overall demand slipped back below pre-Covid-19 levels and most of the indicators for the fundamental drivers of air cargo demand are weak or weakening.

“While the trading environment is tough, there is some good news. Airlines are getting help in managing through the volatility with yields that have remained high and fuel prices that have moderated from exceptionally high levels.

“Looking ahead, with inflation reducing in G7 countries policymakers are expected to ease economic cooling measures and that would stimulate demand.”