No signs of a peak season as air cargo market remains weak in August

07 / 09 / 2023

Source: Shutterstock

Although air cargo declines have narrowed in recent months there are no signs that the industry will enjoy a peak season despite some expressing hopes of a recovery in the final months of the year.

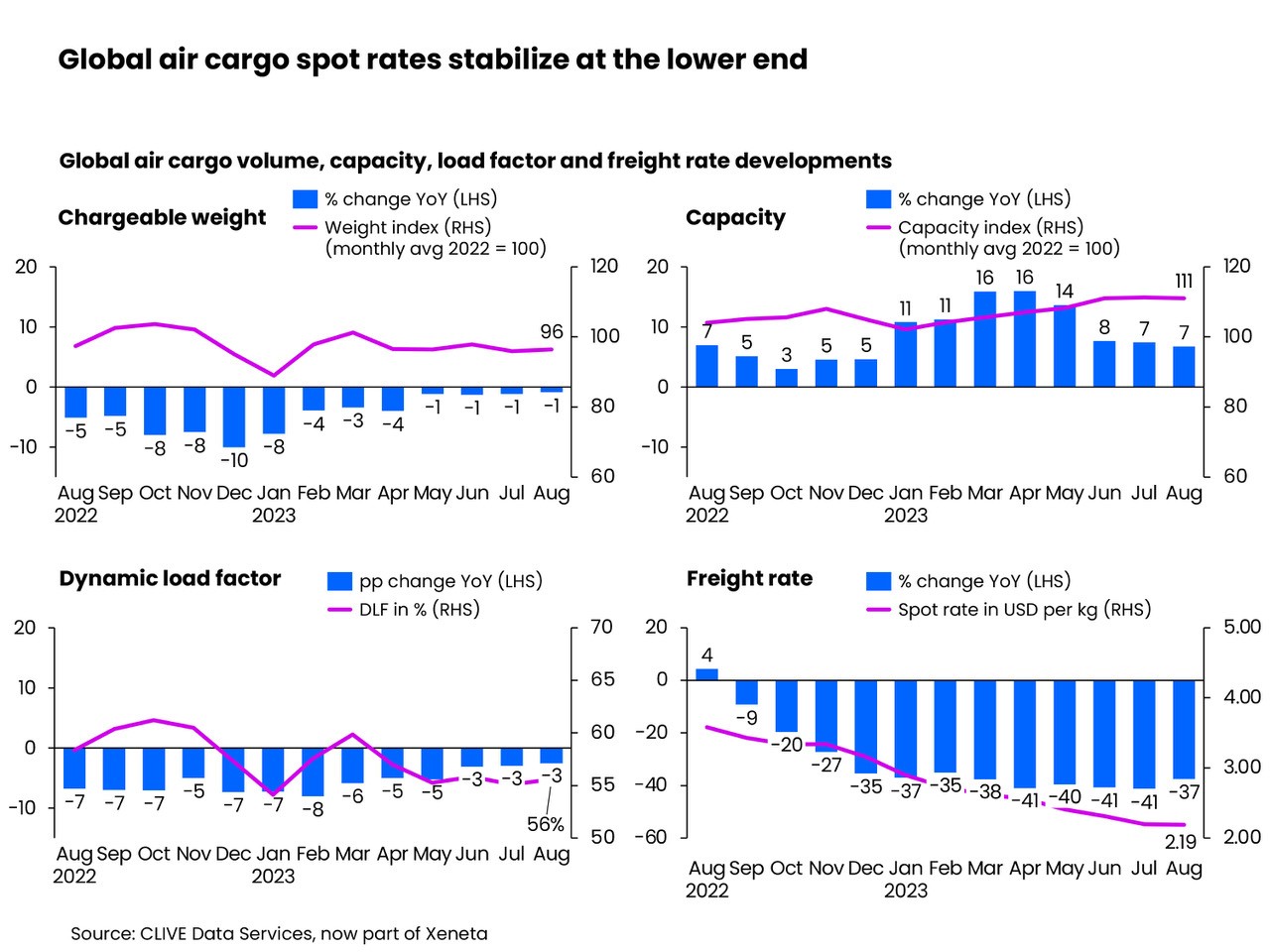

The latest data from Xeneta-owned CLIVE Data Services shows that in August demand in chargeable weight terms declined by 1% year on year for the fourth month in a row – an improvement at least on the first four months.

Capacity for August was up by 7% on last year and the dynamic load factor – taking into account both volume and weight – improved by three percentage points to 56%.

While volume declines have narrowed as the year has progressed, Xeneta chief airfreight officer Niall van de Wouw said that the latest figures undermine reports of a volume spike in August and hopes of a demand pick-up over the final four months of 2023.

Van de Wouw pointed to the slow ocean market, which tends to have its peak season in September, as a signal of things to come for air cargo.

“We are picking up signals that it could take another few quarters before we see more demand on a global level,” said van de Wouw.

“August was very quiet, like July, and we see no meaningful signals from a qualitative or quantitative point of view of any kind of peak arising this year.

“There might be some early peak season charter requests floating around but they are backed up by very little demand.

“The (low) rates and the limited timeframe that the requestors are looking for signal that they are not too concerned at the moment about getting the required capacity when they actually need it.

“The market seems to have levelled out, but still holds a lot of uncertainty, and not just for airfreight.

“There was also no peak for the ocean market, which typically precedes the airfreight market by a couple of months.

“There are even blank sailings scheduled ahead of the Golden Week period.

“There is likely to be upward pressure on airfreight rates in the second half of October as capacity is taken out of the market, but it’s getting late in the game to positively impact the industry’s 2023 performance, and the signals for the rest of the year are not good given the macroeconomic outlook hasn’t improved.”

Recently, Etihad Cargo head of revenue management, fleet and network Leonard Rodrigues said that charter prices for the fourth quarter are already up by around 20-25% compared with the third quarter – last year there was no increase in charter prices between the two periods.

He expected there to be “some level of peak because some people will need 100-tonne capacity and the charter prices are already increasing”.

However, he added: “Whether it will extend to an overall ad hoc market that fights against each other for the last pallet capacity on every flight, it doesn’t seem like it at the moment.”

Van de Wouw said he expected the slower air cargo market to result in more long-term deals being struck by shippers.

“Whichever way you choose to look at it, demand growth simply does not exist in this current moment or for the foreseeable future.

“Shippers will no doubt be tempted to fix more longer-term deals because the levelling of volumes and the imminent drop-off of some capacity means the market may not get any better than it is right now for capacity buyers.”

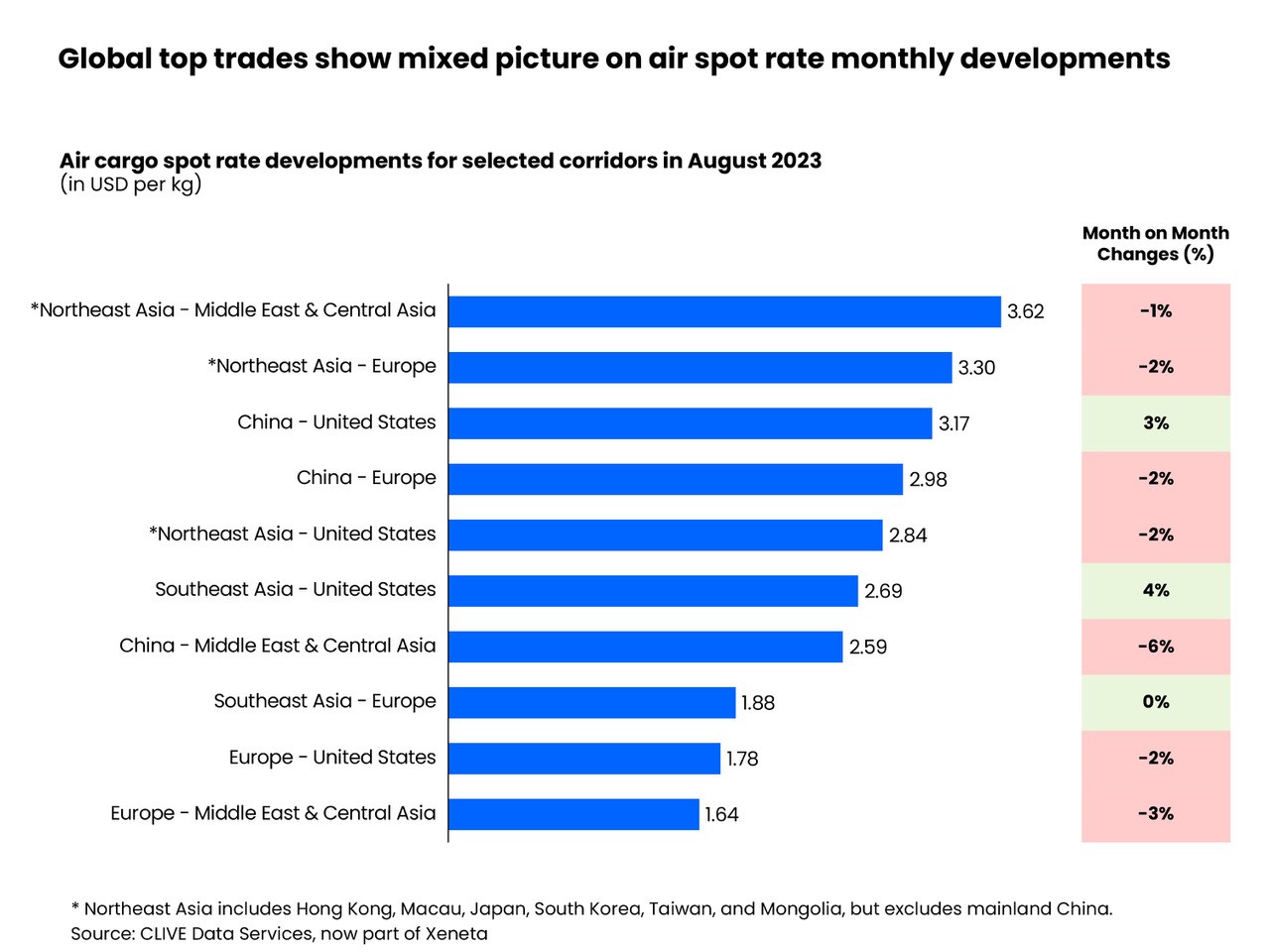

CLIVE’s data showed that spot rates declined 37% year on year to $2.19 per kg in August and down slightly on the $2.20 achieved in July.

The data provider said that of the 10 major trade lanes assessed in the past month, only China-US and Southeast Asia-US recorded growth, with air cargo spot rates up 3% and 4% respectively on these corridors.

“This is attributed to a more resilient US economy with strong retail sales and, to some extent, also delayed recovery of US-China passenger bellyhold capacity, which is growing at a much slower pace than Europe-China,” CLIVE said.

“Even so, due to capacity shortage triggered by various geopolitical issues, airfreight spot rates ex Northeast Asia to Middle East & Central Asia, Northeast Asia to Europe, China to the US and China to Europe remained highly elevated, still up by around 55% from their pre-pandemic levels.”