Top 25 cargo airlines: Freighter operators to the fore

04 / 08 / 2021

Copyright: Shutterstock

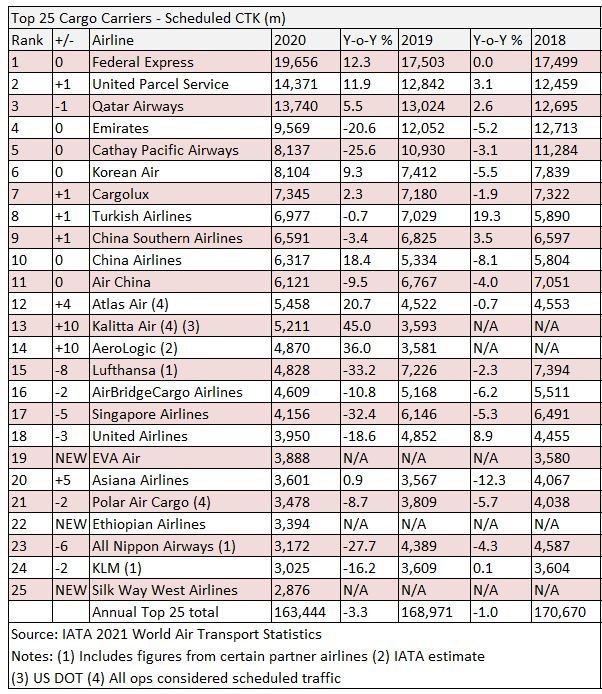

FedEx, UPS and Qatar were last year the largest air cargo carriers once again, but there were major winners and losers in the overall top 25 airlines as the Covid pandemic took its toll on the market (see full at end of article).

According to IATA’s latest World Air Transport Statistics report, the top 25 cargo airlines last year saw traffic in scheduled cargo tonne km (CTK) terms decrease by 3.3% year on year, which is better than the overall industry decline of 9.1%.

IATA says the decline in demand was down to supply chain disruption caused by strict lockdowns, the lack of belly cargo capacity due to the grounded passenger fleet as well as the direct impact of lockdowns on demand.

However, it adds that the easing of lockdowns starting in May, e-commerce growth and the strength of manufacturing activity helped air cargo to rapidly recover as the year progressed.

Topping the list was once again US express giant FedEx which saw its volumes increase by 12.3% year on year to 19.7bn CTK.

The express firm benefitted from increased e-commerce volumes – as shoppers switched to online ordering in light of Covid lockdowns – and a resurgent US economy.

According to the WATS report, North American carriers benefitted from a 4.5% year-on-year increase in CTKs – the best performance of any region.

The only other region to see its airlines record a growth in cargo traffic last year was Africa, with carriers from the region noting a 1.8% increase in CTKs compared with a year earlier.

“Strong fiscal stimulus in the US boosted demand for goods manufactured in Asia, allowing CTKs carried by North American airlines to grow 4.5% year on year,” IATA said.

“This did not benefit Asia Pacific to the same extend, partly because traffic within the region was weak. CTKs in Africa grew by 1.8%, due to the less stringent lockdowns and control measures there.”

Second placed UPS also benefitted from the resurgent US economy and the boom in e-commerce demand as its cargo traffic increased by 11.9% to 14.4bn CTK.

The improvement was enough to leapfrog Qatar Airways, which would have been affected by fewer passenger flights, into second place.

Despite the impact of Covid on its bellyhold network, Qatar still managed register a 5.5% increase in cargo traffic to 13.7bn CTK as it outperformed many of its combination carrier rivals.

One point to note on the IATA statistics is that they only include scheduled services and not charter operations.

While there are always a large number of charter flights, the Covid pandemic has resulted in a large increase in charter flying, which could have affected rankings if an airline targeted charter at the expense of scheduled more than in the past.

Another notable trend was the success of airlines with large freighter fleets compared with bellyhold operators and combination carriers.

The highest climbers, for example were Kalitta Air and Aerologic, which both jumped 10 places on the back of a 45% and 36% increase in demand respectively.

Other airlines to report double-digit percentage increases in demand were China Airlines with an 18.4% increase and Atlas Air which registered a 20.7% jump in demand.

In contrast to airlines with large freighter fleets, British Airways, Air France and American Airlines all dropped off the list.

The carrier that dropped the most places in the top 25 was Lufthansa as it registered a 33.2% year-on-year decrease in demand and slipped eight places to 15.

In the process it lost its position as the highest ranking German airline in the list to Leipzig-based AeroLogic.