Top 25 air forwarders 2016 revealed: DHL maintains top spot

28 / 06 / 2017

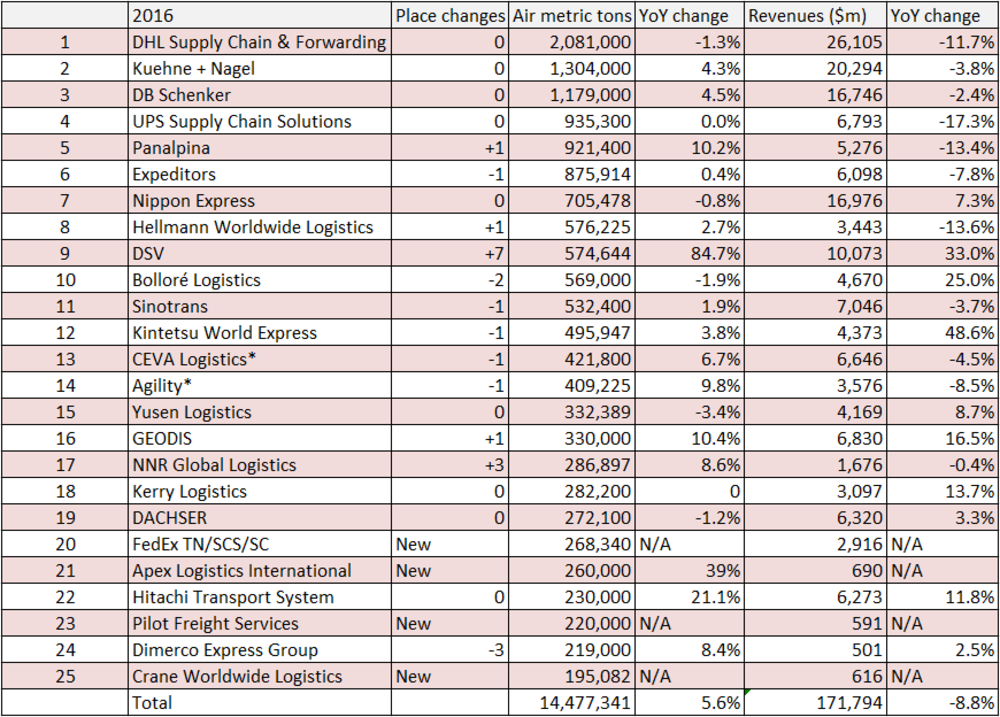

DHL Global Forwarding, Kuehne+Nagel (K+N), DB Schenker and UPS maintained their position as the leading four airfreight forwarders in 2016, while DSV’s acquisition of UTi propelled it up the list (scroll to end for full list).

The latest top 25 Global Freight Forwarders list from consultant Armstrong & Associates, based on estimates by the firm’s analysts and reported figures, revealed that while the leading forwarders enjoyed air cargo volume growth last year, revenues came under pressure.

Overall, airfreight demand at the top 25 forwarders increased by 5.6% year on year to reach 14.5m metric tons. The overall market is estimated to have increased by around 2% last year, suggesting that the largest players outgrew their medium and smaller rivals.

In contrast, overall revenues declined by 8.8% against 2015 levels to $172bn as a result of air and ocean freight rate pressure, currency fluctuations and lower fuel surcharges.

The largest airfreight forwarder was again DHL Supply Chain and Global Forwarding, despite a decline in air cargo traffic of 1.3% year on year to 2.1m metric tons.

An end-of-year airfreight surge was not enough to offset a selective market strategy, where it turned away non-profitable volumes.

This selective strategy has now come to an end and the forwarder should, especially given the strong market conditions registered so far this year, see airfreight demand improve in 2017.

During the first quarter of 2017, the company registered a 12.2% year-on-year improvement in air tonnages to 534,000 tonnes.

The forwarder blamed the decline in revenues on lower demand, lower sea and air rates, lower fuel surcharges and currency effects.

K+N, meanwhile, continued to close the gap on DHL, although it still lags far behind its German rival.

The Switzerland-headquartered firm saw air cargo traffic increase by 4.3% year on year to reach 1.3m metric tons.

The forwarder said that the improvement was down to its industry-specific airfreight solutions, such as KN EngineChain, a specialised service package for production and spare parts logistics as well as the maintenance of aircraft engines.

“K+N’s leading solution for temperature-sensitive goods, pharmaceutical or perishable products, generated significant new business. The improved margins and operational efficiency led to further growth in profitability,” it said in a statement.

K+N also benefitted from an end-of-year surge in demand, which saw airfreight volumes increase by 10.4% in the final quarter of the year.

Revenues were also down at K+N as it also felt the effect of lower rates, lower fuel surcharges and currency effects.

Third placed DB Schenker pointed out that it managed an increase in airfreight demand, of 4.5% year on year to 1.2m metric tons, despite 2015 receiving a boost from the closure of seaports on the US west coast, which forced shippers to turn to airfreight.

“In 2016, volumes were driven by perishable goods, industrial intermediates, chemicals and consumer goods, with virtually all sectors recording stagnating or declining development,” the German forwarder said.

“The special effect from 2015 resulted in a strong decline on the transpacific trade route in particular, whereas volumes increased further between Asia and Europe.

“A particular increase was witnessed on the trade route from the Near/Middle East–Europe.”

The fastest grower in the list was Danish company DSV.

It climbed seven places to become the ninth largest airfreight forwarder, with volumes increasing by 84.7% compared with 2015 to 574,644 tonnes.

The improvement is largely due to its acquisition of UTi, which finished 2015 as the fifteenth largest airfreight forwarder.

DSV said that the market was boosted by certain one-off events in the second half of 2016: disrupted supply chains following the financial collapse of Hanjin and a high activity level, especially in Asia.

The market was characterised by “periods with overcapacity and intense competition, but also peaks with lack of capacity”. This resulted in highly volatile freight rates.

Revenue growth lagged behind airfreight volume improvements as a result of the volatile market and also because of UTi’s strength in airfreight compared with seafreight.

Panalpina also saw airfreight demand improve by a double-digit percentage as it registered a 10.2% improvement to 921,400 metric tonnes.

An acquisition was also behind this company’s improvement as its purchase of Kenya-based Airflo, which specialises in perishables, compensated for declines in its oil and gas business.

The company has continued on the acquisition trail this year with the purchase of Danish firm Carelog and another Kenyan perishables forwarder, Air Connection.

In the first quarter, airfreight demand improved by 8% to 233,000 tonnes. If the forwarder were to continue to grow at this rate it would be on the verge of joining the 1m tonne club with DHL, K+N and DB Schenker.

Another fast growing forwarder was GEODIS, which registered a 10.4% year-on-year improvement in airfreight volumes to 330,000 metric tons.

Again, an acquisition helped fuel growth, as the company acquired forwarder OHL as it expanded its presence in the US.

The second largest increase of the year – in percentage terms – was Apex Logistics, which registered an improvement of 39% to 260,000 metric tons.

In an analysis of the company, Armstrong & Associates said the forwarder’s fastest growing operations were Amsterdam, Netherlands with 261% year-over-year growth, Hong Kong at 76%, and Chicago with 53% growth.

“Apex Logistics has grown rapidly since its founding in 2001 with its core business as an air freight wholesaler,” the consultant said.

“It then quickly increased its service offering expanding into retail air freight forwarding and value-added international transportation management solutions.

“In addition to working with the largest internet retailer, Apex Logistics serves a cadre of Fortune 500 companies. Its target industry segments include e-Commerce, High-Tech, Fashion & Garments, Automotive, Consumer & Pharmaceutical, and Industrial.

“Key customers include: Apple, Hewlett-Packard Company, ASUSTeK Computer, Motorola/Lenovo, Incipio Technologies, AT&T, Jones New York, Barnes & Noble, and Abercrombie & Fitch.

“As part of its e-commerce offering, Apex Logistics is working with customers using both Alibaba and JD.com platforms.”

The only other company to register a double-digit percentage improvement in airfreight demand was Japan-based Hitachi Transport System as it improved by 21.1% to 230,000 metric tons.

In early 2016, the company secured a “capital and business alliance” with SG Holdings and Sagawa Express.

At the other end of the scale, the company to record the largest decline in airfreight volumes was Yusen Logistics with a fall of 3.4% to 332,389 metric tons as the Japanese market continued to come under pressure.

Others to register declines were DHL, Nippon Express, Bolloré Logistics and Dachser.

Revenues and metric tons are company reported or Armstrong & Associates, Inc. estimates. Revenues have been converted to US$ using the average annual exchange rate in order to make non-currency related growth comparisons. Copyright © 2017 Armstrong & Associates, Inc.

* Figures adjusted by Air Cargo News based on company annual reports

Click here to see the 2015 list.

Click here to see the 2014 list.

Are your figures incorrect, or should you have been included on the list? Please email [email protected]