Top 25 airfreight forwarders: Kuehne+Nagel takes top spot from DHL

21 / 06 / 2022

Photo: Atlas Air Worldwide

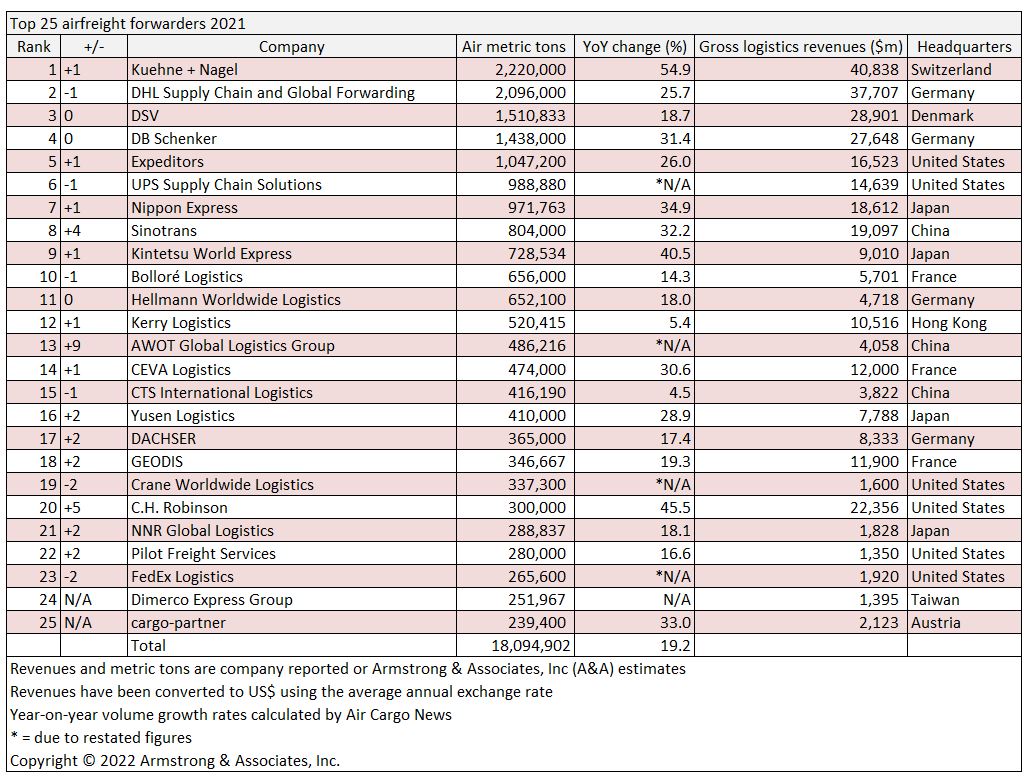

There is no doubt that 2021 was a bumper 12 months for airfreight forwarders with revenues, profits and volumes reaching new highs, but it was also a year of change at the top as Kuehne+Nagel knocked DHL off the top spot (see full list at end of article).

The latest annual statistics from consultant Armstrong & Associates show that Kuehne+Nagel (K+N) was the world’s largest airfreight forwarder in terms of volumes in 2021 as it recorded a 54.9% increase to 2.2m tonnes.

The large increase came as 2021 was a bounce back year following the worst of the Covid pandemic that saw demand fall and large swathes of capacity taken out of the sky as passenger fleets were grounded and cargo carriers had to find new ways to transport shipments.

Demand was also boosted as economies recovered from the pandemic and the public had more cash to spend on goods as services were still limited by the pandemic.

There was also modal shift as the container shipping industry struggled with congestion at ports and container shortages.

K+N also benefited from the acquisition of Apex Logistics. The first-time consolidation in May 2021 of airfreight provider Apex Logistics accounted for around half of the growth.

At the time of acquisition, K+N said Apex handled around 750,000 tonnes of air cargo per year.

“Limited global freight capacity in 2021 called for customised solutions from the Air Logistics business unit,” K+N said. “Demand remained strong for K+N’s services in areas such as pharmaceuticals, essential goods and e-commerce. This enabled the business unit to gain significant market share.”

It added: “In 2021, the increased demand for air transport services was generated from a solid economic rebound but also from challenges in seafreight supply chains; this in combination with an extended period of low availability of belly capacity due to low frequency of passenger travel has led also in the airfreight market to capacity shortage and high freight rates.

“Similar to the situation in seafreight, a favourable service mix, strong development in the trans-pacific market, unprecedented access to charter capacity and operational efficiency under the difficult circumstances contributed to significantly increased margins.”

Overall, the top 25 last saw their air cargo volumes increase by 19.2% to 18.1m tonnes compared with those companies occupying the top 25 spots in 2020 as the industry benefited from the bounce back in both demand and capacity.

Other noticeable came from the Japanese forwarders as they reported above market improvements in air cargo demand, CH Robinson as it recovered from a particularly difficult 2020 and DSV which saw its growth lag behind that of its rivals following on from years of acquisition fuelled growth.

In the first quarter of 2021 the forwarder reported below market growth as it was “impacted by discontinued Panalpina business following the integration”. However, the company recovered later in the year in line with the market.